Many investors turn to dividends to generate a steady income in retirement. Unlike fixed-income securities, dividend stocks offer a combination of current income and capital appreciation. Some dividends are also subject to a lower tax rate than fixed-income securities, making them a more tax-efficient option for investors.

Let’s dive deeper into how dividends work and what every investor should know about dividend taxes.

Dividends are an excellent way to generate income from a portfolio, but there are several tax considerations to keep in mind. Click To Tweet

A Brief Dividend Primer

Dividends are regular payments that companies make to their shareholders. Rather than selling stock to cash in gains, dividend-paying companies enable shareholders to generate a steady income from their portfolios. They also tend to be less volatile than the overall stock market, providing retirement-aged investors extra safety.

Companies may offer several types of dividends:

- Cash Dividends – Cash dividends are the most common type of dividend, where companies make cash payments directly into shareholder brokerage accounts.

- Stock Dividends – Stock dividends occur when companies pay investors additional shares of stock rather than cash, having an effect similar to that of a stock split.

- DRIPs – Dividend Reinvestment Plans, or DRIPs, are opt-in plans that automatically reinvest cash dividends into company stock – often at a discount to the market price.

- Special Dividends – Special dividends are similar to the cash version but don’t occur regularly. For example, a company may distribute profits from a recent asset sale.

- Preferred Dividends – Preferred dividends are payments made to preferred rather than common stockholders. These dividends are typically fixed and paid quarterly.

The amount of dividends you receive depends on how many shares you own. After a company announces a dividend, investors must purchase the stock prior to the ex-dividend date to receive the payout. Investors who buy the stock before and sell after the ex-dividend date will still receive the dividend even if they don’t own the stock at payout time.

You can also invest in dividend stocks using mutual funds or exchange-traded funds (ETFs). In that case, you’ll typically receive dividend payments on a monthly or quarterly basis.

Qualified vs. Non-Qualified Dividends

Before 2003, all dividends were subject to ordinary income tax at the taxpayer’s marginal tax rate. And that meant wealthy taxpayers in higher tax brackets paid a high tax on dividend income.

These investors often pressured companies to choose more tax-efficient ways to return capital, such as stock buybacks. And other companies simply hoarded cash.

The Bush administration introduced qualified dividends in 2003 to remove these quirks in the tax code and incentivize companies to pay dividends. Under the new law, dividends paid by U.S. companies or U.S.-traded companies to shareholders that owned the stock for at least 60 days are subject to the lower capital gains tax rate.

There are also some exceptions to the rule. For example, real estate investment trusts (REITs) and master limited partnerships (MLPs) don’t usually pay qualified dividends. In addition, bond-like securities, like money market funds, and dividends paid out via an employee stock option plan are taxed as ordinary dividends.

The good news is that you don’t have to figure all of this out as an investor. Instead, your broker will determine whether the dividends you receive are qualified or non-qualified on your year-end 1099-DIV.

2022 & 2023 Dividend Tax Rates

All dividend income is subject to taxation, but the amount of tax depends on whether it’s qualified or non-qualified and your income tax bracket.

Qualified Dividend Tax Rates

2022

| Capital Gains Tax Rate | Single | Married Filing Separate | Head of Household | Married Filing Jointly |

| 0% | Up to $41,675 | Up to $41,675 | Up to $55,800 | Up to $83,350 |

| 15% | $41,675 to $459,750 | $41,675 to $258,600 | $55,800 to $488,500 | $83,350 to $517,200 |

| 20% | Over $459,750 | Over $258,600 | Over $488,500 | Over $517,200 |

2023

| Capital Gains Tax Rate | Single | Married Filing Separate | Head of Household | Married Filing Jointly |

| 0% | Up to $44,625 | Up to $44,625 | Up to $59,750 | Up to $89,250 |

| 15% | $44,626 to $492,300 | $44,626 to $276,900 | $59,751 to $523,050 | $89,251 to $553,850 |

| 20% | Over $492,300 | Over $276,900 | Over $523,500 | Over $553,850 |

Non-Qualified Dividend Tax Rates

2022

| Tax Rate | Single | Married Filing Separate | Head of Household | Married Filing Jointly |

| 10% | Up to $10,275 | Up to $10,275 | Up to $14,650 | Up to $20,550 |

| 12% | $10,276 to $41,775 | $10,276 to $41,775 | $14,651 to $55,900 | $20,551 to $83,550 |

| 22% | $41,776 to $89,075 | $41,776 to $89,075 | $55,901 to $89,050 | $83,551 to $178,150 |

| 24% | $89,076 to $170,050 | $89,076 to $170,050 | $89,051 to $170,050 | $178,151 to $340,100 |

| 32% | $170,051 to $215,950 | $170,051 to $215,950 | $170,051 to $215,950 | $340,101 to $431,900 |

| 35% | $215,951 to $539,900 | $215,951 to $323,925 | $215,951 to $539,900 | $431,901 to $647,850 |

| 37% | Over $539,900 | Over $332,925 | Over $539,900 | Over $647,850 |

2023

| Tax Rate | Single | Married Filing Separate | Head of Household | Married Filing Jointly |

| 10% | Up to $11,000 | Up to $11,000 | Up to $15,700 | Up to $22,000 |

| 12% | $11,001 to $44,725 | $11,001 to $44,725 | $15,701 to $59,850 | $22,001 to $89,450 |

| 22% | $44,726 to $95,375 | $44,726 to $95,375 | $59,851 to $95,350 | $89,451 to $190,750 |

| 24% | $95,376 to $182,100 | $95,376 to $182,100 | $95,351 to $182,100 | $190,751 to $364,200 |

| 32% | $182,101 to $231,250 | $182,101 to $231,250 | $182,101 to $231,250 | $364,201 to $462,500 |

| 35% | $231,251 to $578,125 | $231,251 to $346,875 | $231,251 to $578,100 | $462,501 to $693,750 |

| 37% | Over $578,125 | Over $346,875 | Over $578,100 | Over $693,750 |

Taxes on Foreign Dividends

Many investors hold a substantial portion of their portfolio in foreign stocks, so it’s important to understand how taxes work on dividends from these holdings.

While the U.S. government doesn’t withhold dividend taxes for U.S. residents, many foreign governments do withhold taxes on dividends paid to non-resident shareholders.

In some cases, foreign dividend tax withholdings can be significant. For example, Australia, Canada, France, Germany, Ireland, and Japan all have dividend tax withholding rates of more than 20%. The good news is that the U.S. has tax treaties with most countries to reduce these amounts to about 15% in most cases.

You can offset the impact of foreign taxes on dividends using a foreign dividend tax credit or deduction. If your federal tax withholdings are $300 or less (or $600 filing jointly) and you’ve received a 1099-DIV from your broker, you can claim the entire withholding amount as a tax credit, which effectively eliminates the foreign dividend tax.

How to Report Dividend Income

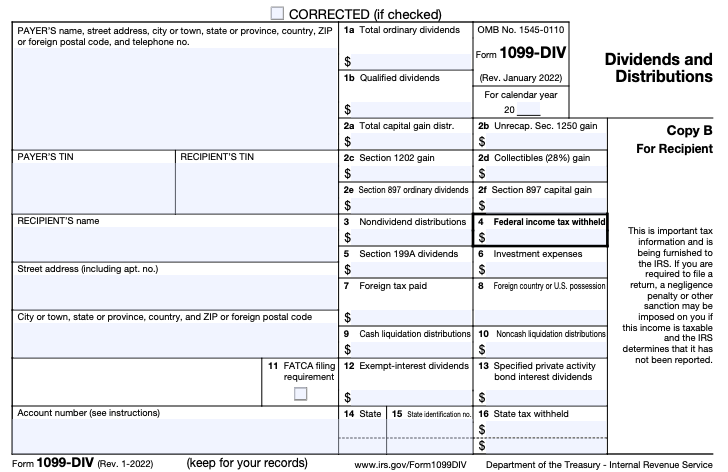

The rules surrounding dividends may seem complex, but the good news is that brokers are responsible for figuring everything out. Brokers will provide you with a Form 1099-DIV – or sometimes a Schedule K-1 – at the end of each year if you receive more than $10 in payments. These forms will specify whether they are qualified or non-qualified.

Form 1099-DIV breaks down all of the information you need to file each year. Source: IRS

Using the information on these forms, you can report dividend income on Line 3b of Form 1040. And, if you received more than $1,500 of taxable ordinary dividends, you must also report these dividends on Schedule B. You may also receive other types of distributions subject to different rules, such as the 28% collectibles tax or real estate capital gains.

In addition to federal taxes, many states tax dividends as ordinary income or capital gains. That said, nine states – Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming – have no state income tax. However, New Hampshire taxes interest and dividends until phase-outs complete in 2027.

The Bottom Line

Dividends are a common way to generate current income from an investment portfolio. In general, short-term dividends are subject to ordinary income tax, whereas dividends from long-term holdings are subject to the lower capital gains tax rate. At the end of each year, your broker will provide you with everything you need to file.

If you’re investing in dividend stocks, TrackYourDividends.com can help you follow the performance, payouts, and diversification of your portfolio. You can also screen for dividend investing opportunities and track DRIPs for a set-and-forget dividend strategy.

Sign up and get started today!

This article was prepared for informational purposes only. TrackYourDividends does not provide tax advice. This article is not intended to provide, and should not be relied on for, tax or accounting advice. You should consult your own tax or accounting professional before engaging in any transaction.